Credit cards - everyone knows and values them. No hotel booking abroad without a credit card: Shopping in the e-shop: With a credit card, it's easy and uncomplicated. All in all, easy, convenient and cashless. The benefits are obvious, but what are the stumbling blocks? We are happy to answer that in this blog.

What kind of credit card models are there?

• Chargeable credit cards (e.g. credit card at your house bank)

• Free credit cards (e.g. Cumulus credit card or Coop credit card)

• Credit cards from neo banks (Revolut)

• Debit credit card with prepayment of credit (house bank, third party provider)

However, none of the models mentioned is free, even if they often advertise it. An analysis of the cost of potential free credit cards can be found below. Even with the paid alternatives, the costs are not always clear. We have listed some costs in the list below.

• Sometimes high annual fees for the credit cards

• High fees for ATM withdrawals in Switzerland and abroad

• Unfavorable exchange rates for foreign currencies (e.g. purchases in foreign currencies)

• Very high lending interest and fees in the event of late payment and / or partial payment

Practically all providers charge a service fee, which some providers with cashback functions partially offset.

This begs the question of whether it is worth using the credit card over and over again - as in the examples above.

Are free Credit Cards really for free?

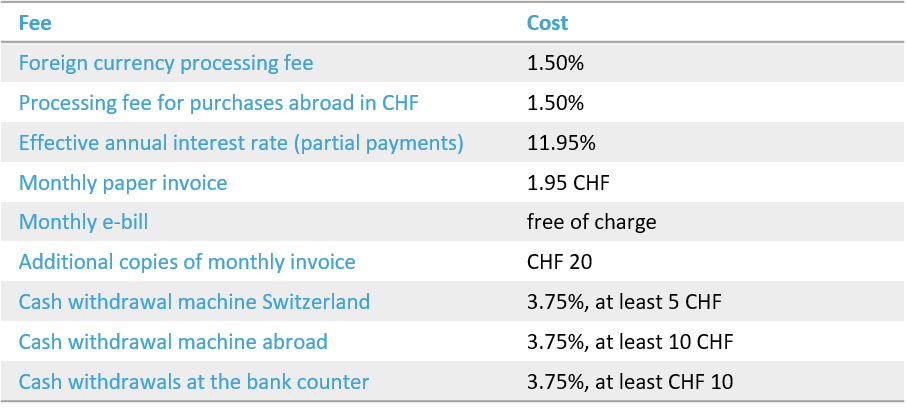

Well over a million customers have a credit card with no annual Migros or Coop fee. Such a card is not free, on the contrary. The fees are communicated less transparently and sometimes even have to be searched for on the website. Below are some examples of costs (using the Cumulus credit card as an example):

Depending on the balance, the installment payment option is certainly important. So we will focus on this point.

What does the installment payment option cost me with credit cards?

Using an open credit card balance, the costs of a partial credit card payment can be shown using a simple example.

Sample calculation:

• Amount open: CHF 10,000.

• Interest: 11.95% per year

• Monthly minimum payment of 5% of the outstanding amount

This results in interest of CHF 853.40 and an open balance of CHF 6'025.- and of course without any further purchases. That means, despite high monthly repayments, just under CHF 4,000 has been repaid after one year. If you want to continue to use the credit card, you can hardly reduce the balance even with regular payments.

Are there any alternatives, or how can I avoid these high partial payment costs?

Yes, there are some alternatives, which of course can be used individually depending on the personal financial situation. Basically, credit card debt is very expensive debt.

Some ways to save money:

• Always pay your credit card bills completely and on time

• Replace credit card debt with a private loan. For example, with a private loan from Crowd4Cash. You benefit from the following advantages:

o Lower interest rates

o Sustainable payment, no unexpected residual debts

o Digital loan application process - 100% online

o Administratively simply with a standing order or LSV at the bank

• Look for support in your private sphere

Do you already have loans and / or credit card debt? Calculate your potential savings by financing with Crowd4Cash (based on a loan of 24months)